Failing to withdraw the minimum amount from retirement accounts results in a hefty federal penalty. eric1513/Getty Images

TSP and Required Minimum Distributions

Rules around these mandatory withdrawals changed under the Secure 2.0 Act.

Required Minimum Distributions are mandatory annual withdrawals from certain retirement accounts, enforced by the federal government once you reach a specific age. These withdrawals apply to traditional IRAs, SEP and SIMPLE IRAs, and employer-sponsored plans like the Thrift Savings Plan. The purpose of RMDs is to ensure that taxes on these previously tax-deferred savings are eventually paid.

If you're still federally employed at the age of RMD commencement, you can postpone RMDs from your TSP until retirement. However, RMDs from other retirement accounts are still necessary. Failing to withdraw the minimum amount results in a hefty federal penalty, although withdrawing more than the minimum is allowed.

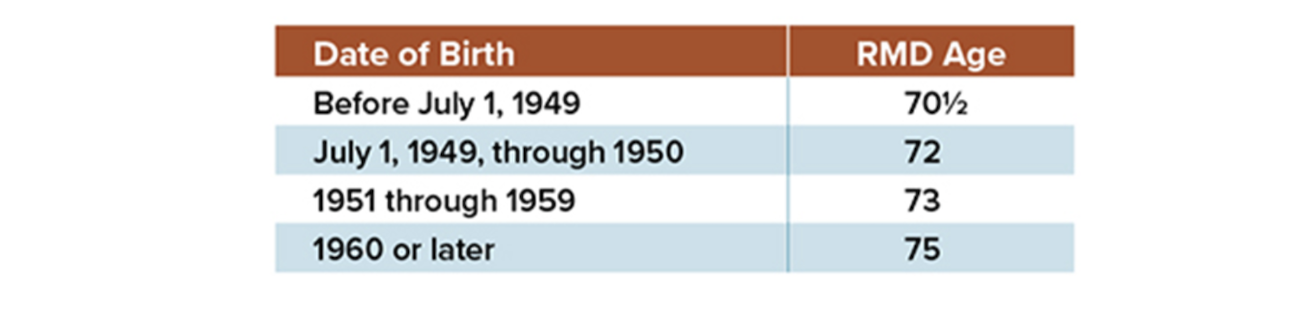

Recent Changes to RMD Rules

The SECURE 2.0 Act has altered the age for beginning RMD’s to:

The penalty for under-withdrawing has been reduced by the SECURE 2.0 Act. Previously, the penalty was 50% of the shortfall, but it has now been lowered to 25%, with the possibility of further reduction to 10% if corrected promptly.

Roth IRAs have always been exempted from RMDs for the account owner and their spouse, a feature that has now extended to the Roth TSP starting in 2024. Non spouse beneficiaries inheriting these accounts, however, are still subject to RMDs. For federal employees, this presents a significant decision in tax planning: Should they continue contributing to their Traditional TSP, which could lead to substantial RMDs in retirement and possibly elevate them to a higher tax bracket when combined with Social Security and pension income, or should they shift their contributions to a Roth TSP, thereby eliminating the concern of RMDs impacting their tax bracket during retirement?

Starting in 2024, surviving spouses who inherit Traditional TSP accounts and are the sole beneficiaries will be treated similarly to those inheriting IRAs. They will have the advantage of using the Uniform Lifetime Table for more favorable RMD calculations and can postpone distributions until they reach their own RMD age or the age at which the deceased would have reached it. In contrast, spouses who inherit Roth retirement plans, including Roth TSPs, will not face any RMD requirements. This change offers a significant tax benefit, especially since surviving spouses will be filing taxes as single, which has a smaller tax bracket compared to the joint bracket. Consequently, a substantial RMD could result in higher tax rates for a single filer than what would have been applied under the joint bracket. In light of this, spouses may want to consider a Roth conversion while they still maintain their joint filing status.

Calculating RMDs:

RMDs are determined by dividing your account balance by a life expectancy factor from IRS tables. You typically use the account balance from the previous Dec. 31. For instance, if you turn 73 in 2024 and have $300,000 in a traditional IRA as of Dec. 31, 2023, your RMD would be $11,321, calculated using the Uniform Lifetime Table.

The IRS permits postponing your first RMD until April 1 of the year after it's due. However, you cannot delay subsequent RMDs past Dec. 31 of the same year, potentially resulting in two RMDs in a single year and affecting your tax liability.

RMDs must be calculated for each retirement plan separately, but when it comes to IRA’s you can choose to withdraw the total amount from one or more IRAs. However, the TSP RMD must be satisfied from the TSP account itself.

Neil Cain is a certified financial planner with Capital Financial Planners. If you don’t feel confident in your tax planning strategy or whether or not you would be better of using Traditional vs. Roth, register for a complimentary check up. For topics covered in even greater depth, see our recorded webinars.

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek guidance from an independent tax or legal professional. The content is derived from sources believed to be accurate. Neither the information presented, nor any opinion expressed constitutes a solicitation for the purchase or sale of any security.