jadamprostore/Getty Images

A closer look at 2025 FEHBP premiums

Open Season is just a few weeks away, and costs are increasing this year. What does that mean for federal employees?

Federal employees and retirees should expect to pay much more for health coverage next year: the enrollee share of FEHB premiums is going up 13.5% on average, which is almost double from last year. OPM cites price hikes from providers and suppliers, more prescription drug usage, and behavioral health spending as the principal drivers for this increase.

How will this impact you this Open Season? I’ll walk you through premium changes in popular plans, discuss which ones saw their costs go up above and below the average, provide enrollment advice for two-person families, and discuss what to expect from FEDVIP options.

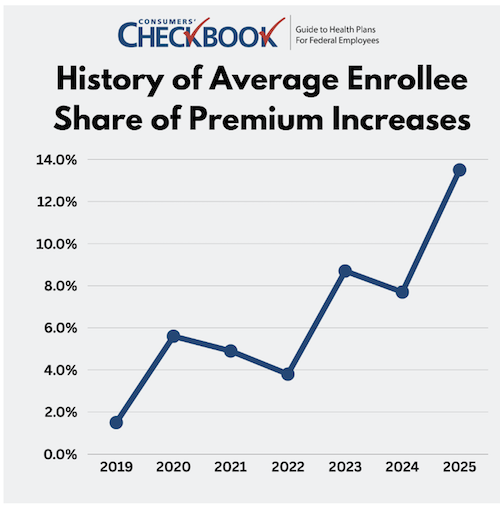

Recent History of FEHB Premium Increases

The 13.5% increase for 2025 marks the largest in recent memory. Just three years ago, the average enrollee increase was only 3.8%. It’s unclear whether 2025 will be an outlier or a trend, but federal employees and annuitants should prepare to pay more going forward and anticipate large premium increases in the future.

How FEHB Premiums are Changing in 2025

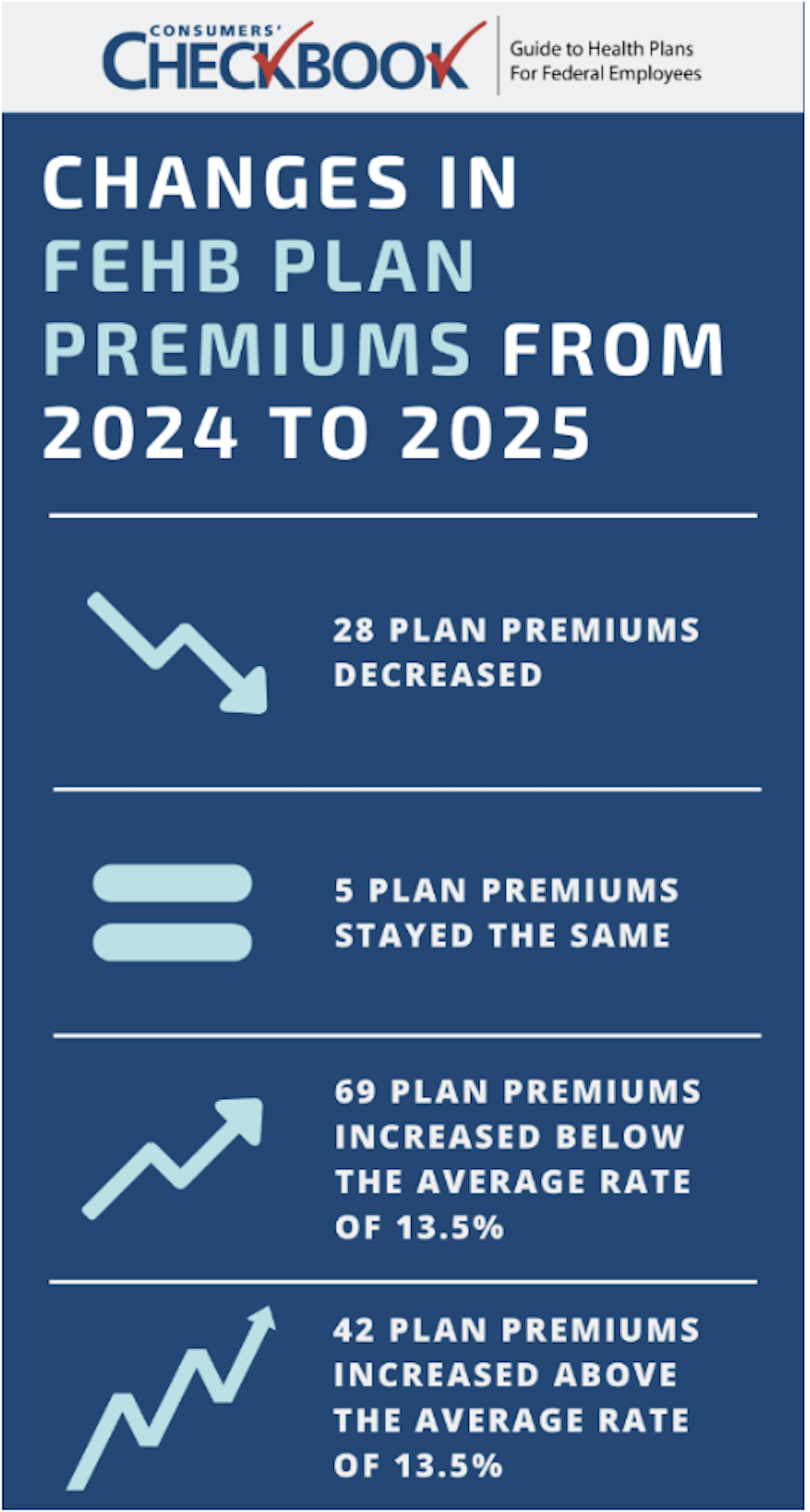

While the average enrollee share of premium is going up, not all plans reflect that trend. For the 144 FEHB plans available in 2024 and 2025, self only premiums will decrease in 28 plans, stay the same in 5 plans, increase below the 13.5% average in 69 plans, and increase above the average in 42 plans.

Some of the changes are striking: the largest decrease in enrollee share of premium is from Presbyterian Health Plan Standard (PS), available in New Mexico, which is 23% lower in 2025, saving self-only enrollees around $732 next year. Carefirst BlueChoice Blue Value Plus (B6), available in the Washington D.C. area, has the same premium in 2025 as 2024. The largest percentage increase is from Health Alliance HMO Standard (K8), available in several states, which is 66% higher in 2025 and will cost self-only enrollees $2,222 more next year.

How is your plan’s premium changing next year? Even if you’re happy with your existing coverage, it will likely be more expensive in 2025. Not all premiums increased at the same rate, and there may be new plan bargains available to you, which is why it’s important to know how this for-sure expense will impact your budget next year.

Blue Cross Blue Shield

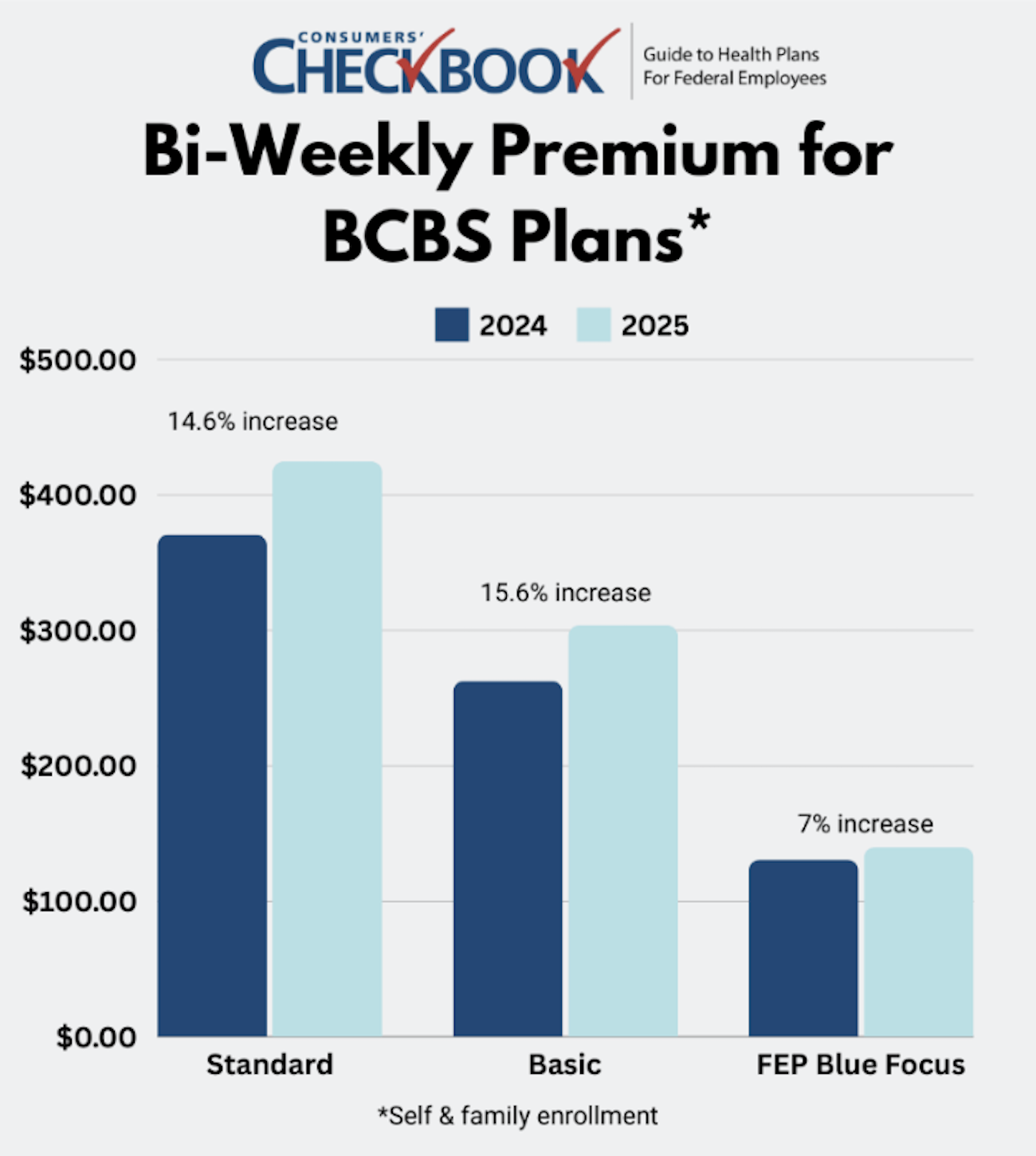

About two-thirds of federal employees are enrolled in one of the Blue Cross Blue Shield (BCBS) plans—Basic, FEP Blue Focus, or Standard.

Both Basic and Standard increased above the all-plan average, and while FEP Blue Focus also went up, it was well below the average.

If you’re currently enrolled in a BCBS plan, when was the last time you evaluated the other two options to compare benefit and cost differences? This upcoming Open Season is a good opportunity to assess whether your current plan is still the best fit for your needs.

There are many differences between Basic, FEP Blue Focus, and Standard, but some of the most significant are that Standard is the only plan where:

- You can see out-of-network providers,

- Receive mail-order prescription drugs (Basic has mail-order prescription drug coverage only for annuitants with Part B),

- Obtain skilled nursing care benefits,

- And receive IVF coverage, up to $25,000 annually.

If you’re enrolled in Standard and don’t use those benefits, you could save some serious money switching to Basic or FEP Blue Focus, and you’ll get to keep your existing BCBS in-network providers. Families switching from Standard to Basic would save $3,147 in premium next year, and families switching from Standard to FEP Blue Focus would save $7,403.

Self-Plus-One vs Self & Family Enrollment

Married couples and two-person families can enroll as self-plus-one or self and family. Most of the time, self-plus-one is the cheaper enrollment choice, but there are 46 FEHB plans where self-&-family enrollment is less expensive than self-plus-one, and 10 plans where the premiums are the same.

There is a sizable amount of money at stake based on your enrollment decision. For example, a two-person family considering the D.C.-area Kaiser High (E3) plan can save $64.23 bi-weekly enrolling as self-&-family compared to self-plus-one. That adds up to $1,670 annually.

OPM has released a chart that shows which plans have lower self and family premiums. Look for the enrollee share of premium and choose the enrollment option that is cheaper. You’ll receive the same plan benefits regardless of enrollment type.

FEDVIP Premiums

FEDVIP premiums have historically increased at a much lower rate compared to FEHB plans. For 2025, FEDVIP dental plan premiums will increase 2.97% on average, and FEDVIP vision plan premiums will increase by .87%.

The Final Word

Your FEHB premium will most likely go up in 2025, and most likely by quite a lot. The 13.5% increase is only an average, and many plans will cost more. While only one factor in your overall plan selection decision, the premium is important because it’s a for-sure expense. You absolutely must check to see how yours is changing for 2025 and consider whether another plan is a better value for you and your family. The 2025 FEHB Open Season starts Nov.11 and ends Dec. 9.

Kevin Moss is a senior editor with Consumers’ Checkbook. Checkbook’s 2025 Guide to Health Plans for Federal Employees will be available on the first day of Open Season, Nov. 11. Check here to see if your agency provides free access. The Guide is also available for purchase and Government Executive readers can save 20% by entering promo code GOVEXEC at checkout.