seng kui Lim/500px/Getty Images

Health Savings Account contribution limits to rise in 2025

Federal employees looking for ways to save on out-of-pocket healthcare costs might benefit from using a high deductible health plan with an HSA.

The IRS announced higher HSA contribution limits for 2025 earlier this month. Self-only enrollees can contribute up to $4,300, $150 more than last year, and self-plus-one and self & family enrollees can contribute up to $8,550, a $250 increase from last year.

To have an HSA, you must enroll in a high deductible health plan. Federal employees looking for ways to save on out-of-pocket healthcare costs, whether those expenses are expected soon or far into the future, can enroll in an HDHP and benefit from the HSA’s triple tax-advantaged saving power.

How FEHB HDHPs Work

HDHPs, as the name suggests, have much higher deductibles than most HMO or PPO plans. Before you meet the deductible, you’ll pay the full allowed charge for the medical service. After you meet the deductible, you’ll pay just a percentage of the service cost. This is referred to as coinsurance, and it ranges between 5-20% depending on the plan.

To help with out-of-pocket costs, either before or after the deductible, HDHPs fund the HSA with monthly premium pass throughs. The HSA contribution amount varies by plan, but ranges from $750 to $1,200 for self-only enrollees and between $1,500 to $2,400 for self-plus-one and self & family enrollees.

Preventive services are free in HDHPs before and after the deductible, and HDHP premiums tend to be lower compared to other popular FEHB plans. The combination of the plan-funded HSA and lower premiums make HDHPs one of the cheapest plan types available to federal employees.

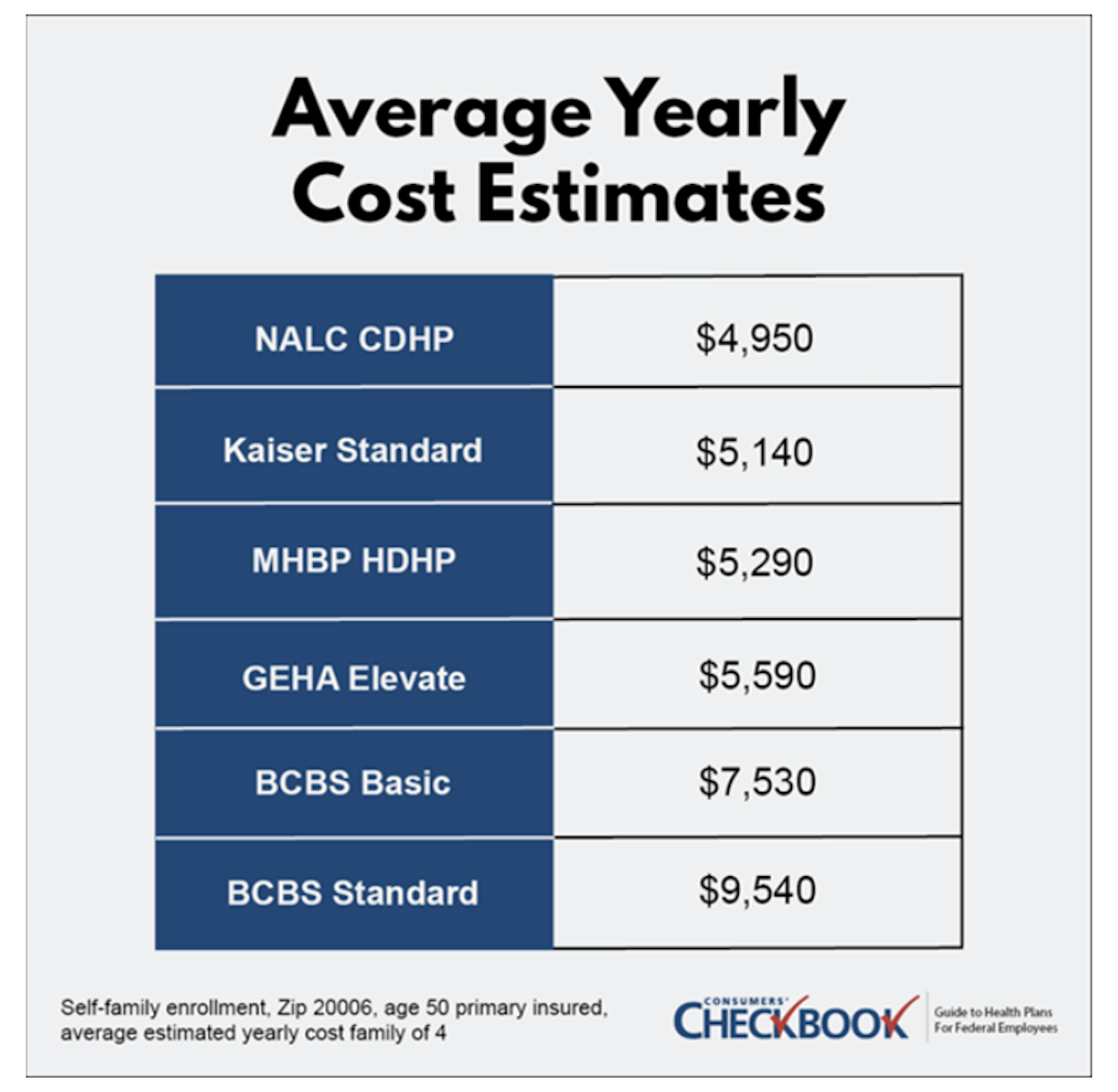

Checkbook’s Guide to Health Plans ranks FEHB plans on estimated yearly cost—the combination of the for-sure expense of premium plus expected out-of-pocket costs based on user information. The chart below shows plan year 2024 yearly cost estimates for a family of four with average healthcare expenses in the Washington, D.C., area. Depending on your current plan, you could save thousands of dollars annually by switching to an HDHP.

HSA Basics

Besides the plan’s monthly contributions, you can choose to make your own. Keep in mind that the higher limits in 2025 include both voluntary and plan contributions. If you’re over the age of 55, you qualify for catch-up contributions that allow for an extra $1,000.

HDHPs choose a financial service company to manage the HSA. You can invest your HSA funds and have access to investment options like you’d see from an individual retirement account. However, if you want to pay for a qualified healthcare expense with your HSA, you’ll need available funds that aren’t invested.

Voluntary HSA contributions are triple tax-advantaged:

- You can make HSA contributions as payroll deductions or as lump sum deposits. Payroll deductions happen pre-tax, lowering your taxable income. Lump sum deposits can be claimed when you file your taxes.

- If you choose to invest your HSA funds, any interest or earnings are tax-free.

- Withdrawals are tax-free when used for qualified healthcare expenses.

Non-medical distributions are allowed with an HSA, but if you’re under 65 you’ll pay a 20% income tax penalty plus your normal tax obligations.

For those thinking about retirement, the HSA can be considered a flexible retirement account that can be used anytime to pay for healthcare expenses tax-free, or as another stream of income in retirement to be used on anything, taxed at your normal rate.

Finally, HSAs are fully portable. If you enroll in an HDHP and later decide to switch to a different plan, you’ll retain ownership of your HSA account and be able to use funds for qualified healthcare expenses.

How to Maximize Your HSA

If you’re enrolled in an HDHP with an HSA, you can’t have a healthcare Flexible Spending Account (FSA). However, we recommend signing up for a Limited Expense Health Care Flexible Spending Account, which can only be used for qualified dental and vision expenses. This will help preserve your HSA balance.

If you switch from a more expensive plan to an HDHP, it might be tempting to pocket the premium difference. Instead, contribute it into the HSA. By doing so, you can use the voluntary contributions for out-of-pocket healthcare expenses without having to touch the plan contributions.

Federal employees are on borrowed time. Once you retire and have Medicare, you can no longer make voluntary contributions into the HSA. HDHPs that typically have an HSA will offer annuitants with Medicare a Health Reimbursement Account instead.

The Final Word

HDHPs are one of the cheapest FEHB plan types for federal employees. Before deciding to enroll in one, carefully consider your predicted healthcare expenses and make sure to check the provider directory found on the plan website to see if your current doctors will be in-network.

Families with large known healthcare expenses, such as orthodontic services for a child or a federal employee wanting to save \for future Medicare Part B premiums, are just two of many examples where having an HSA would be beneficial.

With higher contributions limits in 2025, more than twice FSA limits, federal employees can save even more in an HSA to help pay for healthcare expenses today, tomorrow, and well into the future.

Kevin Moss is a senior editor with Consumers’ Checkbook. Watch more of his free advice and check if the Guide to Health Plans for Federal Employees is available for free from your agency. You can also purchase the Guide and save 20% with promo code GOVEXEC.