Research by

Sponsored by

Building Your Best Future: Federal Long Term Care Considerations

StartAs more and more federal employees reach retirement eligibility, the realities of age and health are becoming increasingly pressing concerns. The potential need for long term care is an essential part of that conversation — so let’s talk about it.

In this card stack, Government Business Council, the research arm of Government Executive, presents a snapshot of the financial, health, and emotional considerations associated with federal long term care.

Contents

- Long Term Care 101

- Mythbusting: "But I'm Too Young for Long Term Care!"

- Mythbusting: "My Family's Got This"

- Mythbusting: "I'll Just Rely on Medicare"

- Mythbusting: "Okay, What About Other Programs?"

- Mythbusting: "I Can Save Enough on My Own"

- Ready...or Not? Federal Employees and Long Term Care

- Considering Long Term Care Insurance

- Long Term Care Insurance: Next Steps

- Start Over

9/9

Long Term Care Insurance: Next Steps

So, it’s time to pull the trigger and buy your long term care insurance. But where do you buy and who from? Most people can buy long term packages directly from their insurance agent, financial planner, or broker. Those are all viable options.

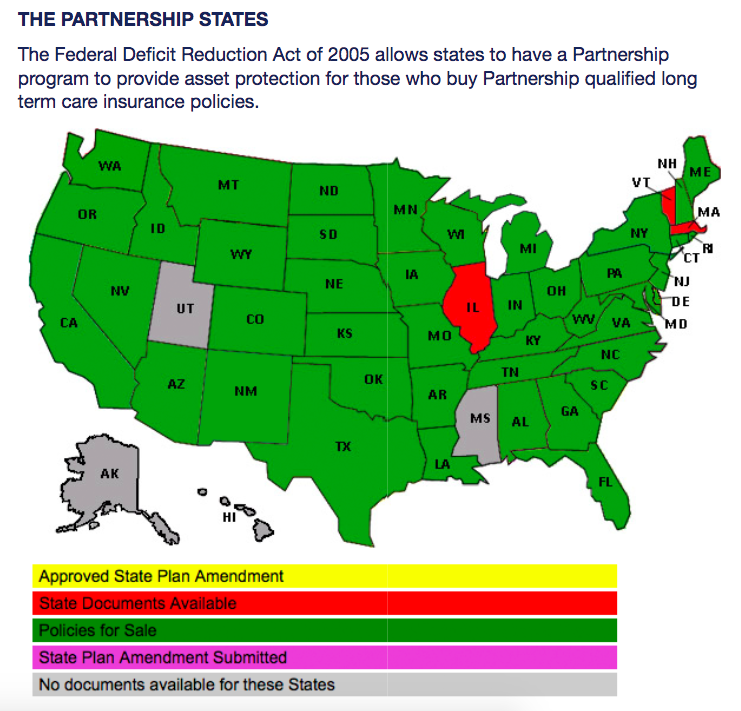

However, residents in some states may be able to attain coverage through a State Partnership Program that links special Partnership-qualified (PQ) policies provided by private insurance companies with Medicaid. These PQ policies:

- Help people purchase shorter-term, more complete long term care insurance

- Include inflation protection

- Allow you to apply for Medicaid under modified eligibility rules if you continue to to need long term care and your policy maximum is reached

- Include a special “asset disregard” feature that allows you to keep assets like personal savings above the usual $2,000 Medicaid limit

Many private and public employers, including the federal government and some state governments, also provide group long-term care programs as a voluntary benefit. While employers do not generally contribute to the premium cost under these programs, they are frequently open to negotiating a favorable rate for you. If you’re already employed, it may be easier to qualify for long term care insurance through your employer than it is to purchase on your own.

And for those of you employed by the Federal government, you already have a long term care option available: the Federal Long Term Care Insurance Program (FLTCIP). Sponsored by the Office of Personnel Management (OPM), FLTCIP was designed specifically to meet the long term care needs of federal employees.