Mohamad Faizal Bin Ramli/Getty Images

Weighing the costs and trade-offs of suspending FEHB for Medicare Advantage

COMMENTARY | An analysis of two markets shows some commercial plans provide the lowest estimated yearly costs, but federal annuitants must consider the required trade-offs like prior authorization and provider access.

Tucked away in Section 9 of every Federal Employee Health Benefits plan brochure is an important and sometimes overlooked provision: “If you are an annuitant or former spouse, you can suspend your FEHB coverage to enroll in a Medicare Advantage plan, eliminating your FEHB premium.”

For annuitants enrolled in Medicare Parts A and B, Checkbook’s Guide to Health Plans compares costs for both FEHB and Medicare Advantage (MA) plans offered by carriers where you keep your FEHB enrollment and continue paying its premium. What we have not previously analyzed is the third option available to federal annuitants: suspending FEHB to enroll in a private, commercial MA plan.

This gap has always raised a question for us at Checkbook:

How does suspending FEHB to enroll in a commercial MA plan compare with FEHB coverage with Medicare as primary, or MA plans offered by FEHB carriers?

To answer it, we selected two geographic markets, gathered benefit and price data for all available commercial MA plans and ran them through our yearly cost estimate model. Our goal was to determine which type of coverage delivers the lowest total costs for federal annuitants. Here are the results, which were first released in the May 2026 NARFE Magazine, and some advice if you’re considering enrolling in an MA plan.

Methodology

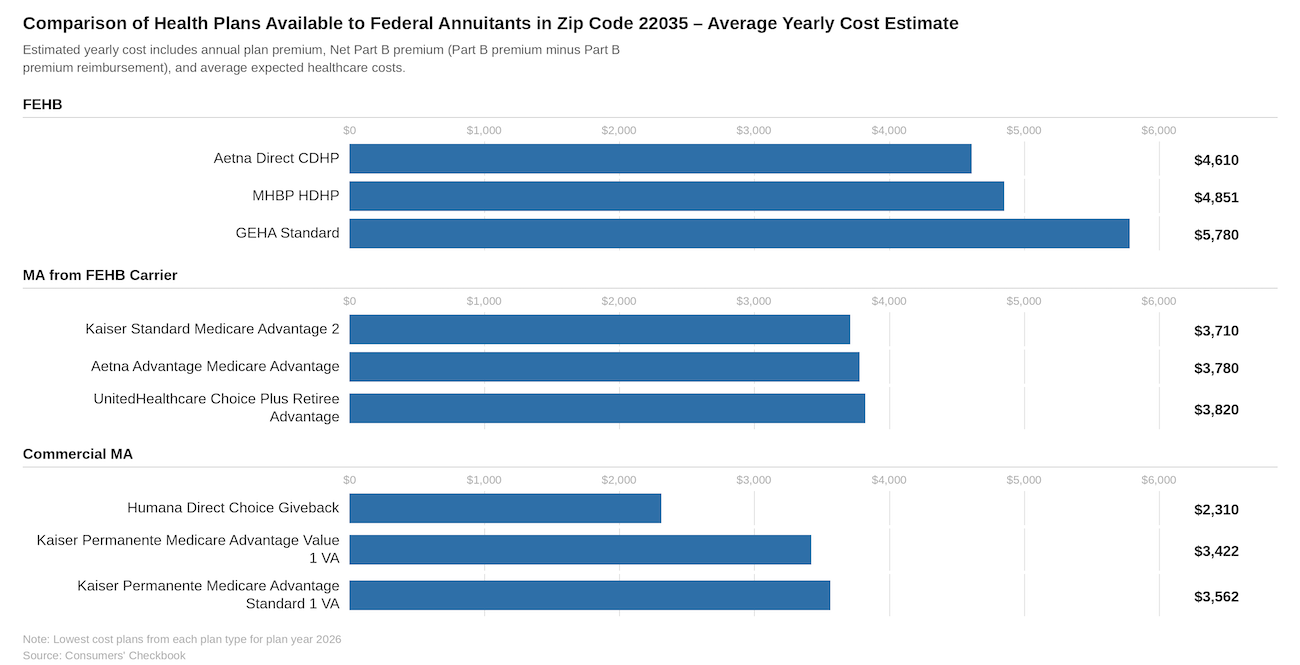

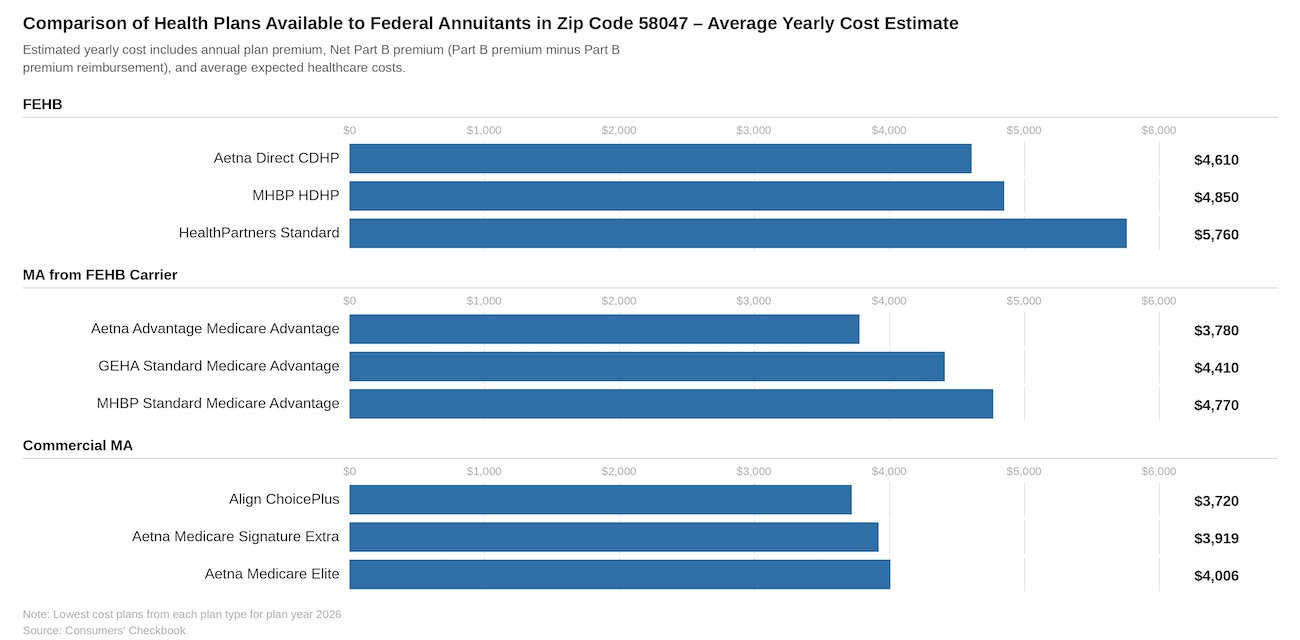

We chose two different geographic locations to perform this research: an area with a high percentage of federal employees and annuitants, Fairfax County, VA (ZIP code 22035), and a rural location, Cass County, ND (ZIP code 58047).

For the three plan types available to federal annuitants — FEHB plan, MA plan from an FEHB carrier, commercial MA plan — we applied the same user profile to calculate yearly cost estimates. The profile is a 65-year-old federal annuitant enrolled in Medicare Parts A and B with income below $109,000 and not subject to Part B or Part D Income Related Monthly Adjustment Amounts (IRMAA), who expects average health care expenses in 2026.

The three lowest-cost health plans for average expected health care costs were used to compare plan options. To see a full ranking on estimated yearly costs for FEHB plans and MA plans from FEHB carriers, visit the Checkbook Guide.

Cost comparison between the three plan types

In Fairfax County, VA, if you have coverage through your FEHB plan with Medicare as primary, Aetna Direct CDHP, MHBP HDHP and GEHA Standard are the three cheapest options. All eliminate out-of-pocket costs for Medicare Part A and B services, and both Aetna Direct CDHP and MHBP HDHP contribute to savings accounts that annuitants can use for Part B premium reimbursement or any other qualified health care expense.

Compared to FEHB plans, MA plans from FEHB carriers can cost less. A federal annuitant could save about $900 a year by enrolling in Kaiser Standard Medicare Advantage 2 instead of Aetna Direct CDHP.

However, the cheapest option in this area is from a commercial MA plan, Humana Direct Choice Giveback. It has the lowest estimated costs because it has no premium and some Part B premium reimbursement, which only leaves out-of-pocket costs for medical services and the remainder of the Part B premium. Compared to federal annuitants who have coverage through their FEHB plan with Medicare as primary, choosing Humana Direct Choice Giveback would save you around $1,400 over Kaiser Standard Medicare Advantage or $2,300 over Aetna Direct CDHP.

In North Dakota, which has fewer MA plans available, there are potential savings with commercial MA plans, but they’re much smaller than what we found in Fairfax County, VA. Federal annuitants could enroll in Align ChoicePlus and save about $60 in estimated yearly costs compared to Aetna Advantage Medicare Advantage, or around $900 compared to Aetna Direct CDHP.

Commercial Medicare Advantage plan advice

In the two geographic markets we researched, a commercial MA plan was the cheapest plan option, but that may not be true where you live. Consider the following before suspending your FEHB coverage and enrolling:

Prior authorization

MA plans could have more requirements, leading to delays in accessing care and an increased risk of claim denials. According to the Commonwealth Fund’s most recent State Scorecard on Medicare Performance, many MA plans require prior authorization even for routine preventive services or specialist visits. It varies significantly by state, from as few as 8.3% of MA plans in South Dakota to as many as 73.1% of plans in Washington.

You’ll need to review the MA plan’s summary of benefits or evidence of coverage for more details on prior authorization.

Provider access

MA plans may have narrower provider networks compared to some FEHB plans. Check to see if your doctors will be in network on the carrier website before enrolling in any MA plan.

No family coverage

Unlike both FEHB and MA plans offered by FEHB carriers, commercial MA plans are individual enrollments. If you need to cover a spouse or a dependent child, you won’t be able to use this option.

Higher out-of-pocket costs

Unlike most MA plans offered by FEHB carriers, where most out-of-pocket medical costs except for prescription drugs are waived, commercial MA plans still have them. And while many have no or very low premiums, you’re trading those savings for higher out-of-pocket costs when you use health care services. As a result, if you have higher health care expenses, the cost savings would evaporate and you’d likely pay more in one of these plans compared to FEHB options.

Higher catastrophic limit

If you have a worst-case health expense year, the higher catastrophic limit may mean you’ll pay more in a commercial MA plan compared to most FEHB or MA plans offered by FEHB carriers. For example, in Fairfax County, VA, the Humana Direct Choice Giveback catastrophic limit is $9,250 for in-network care, whereas the Aetna Direct CDHP catastrophic limit is $6,000.

The final word

Our analysis shows that MA plans can provide substantial financial savings, with some commercial MA plans offering the lowest overall costs for an average year. The savings vary greatly depending on which plan you’re currently enrolled.

However, these savings come with trade-offs and won’t be the right choice for all federal annuitants. Weigh the financial savings against factors like provider access and prior authorization, which is typically more common in MA plans and can sometimes lead to delays in care or denied claims.

However, the decision to enroll in a commercial MA plan carries far different long-term implications for retirees without employer-sponsored coverage. FEHB offers a unique and powerful safety net: annuitants may suspend FEHB to try a commercial MA plan and, if their needs change, unsuspend FEHB during any future Open Season.

This flexibility matters because FEHB plans are guaranteed issue (you cannot be denied coverage or charged more based on health status). By contrast, in 46 out of 50 states, Medicare beneficiaries who leave Medicare Advantage and wish to enroll in a Medigap plan after more than 12 months lose guaranteed issue protection. At that point, insurers are allowed to medically underwrite, meaning they can raise premiums or deny enrollment altogether based on your health status.

In practical terms, federal annuitants can explore MA without the same risks faced by other retirees. The ability to return to FEHB during any future Open Season represents a significant advantage, one that should be factored into your plan evaluation.

Kevin Moss is a senior editor with the Guide to Health Plans for Federal Employees provided by Consumers’ Checkbook. Watch more of his free advice and check here to see if the Guide is available for free from your agency. You can also purchase the Guide and save 20% with promo code GOVEXEC.

NEXT STORY: TSP funds returned to growth in April