Going Private

How do the public and private sectors really compare when it comes to compensation and benefits?

Just when I thought I had explored most retirement benefits topics in this column, I received an interesting e-mail question:

As a Federal Employees Retirement System employee, I am not locked into my retirement so much as someone who is in the Civil Service Retirement System. I won't/can't retire for at least 10 more years. Question: Is there a calculator that shows how much I would have to make on the "outside" to equal or improve on my potential government retirement?

I don't know of any calculator that compares private sector salaries and benefits with federal pay and benefits. I searched for studies comparing the two sectors and found conflicting conclusions.

The Federal Salary Council says that federal salaries lag behind the private sector by 23 percent. On the other hand, Chris Edwards, director of tax policy studies at the Cato Institute, has used data from the Commerce Department's Bureau of Economic Analysis to conclude that as of 2006, average compensation of civilian federal employees was about twice as high as that of private-sector workers. In this calculation, "compensation" includes wages, salaries and supplements such as employer contributions to social insurance and to pension and health insurance funds.

Since I am not an economic analyst and I don't have the technology expertise to create a calculator, the best I can do is provide a snapshot of federal benefits and allow you to compare them to what you might find in the private sector. (Note: Since all new employees are hired under the Federal Employees Retirement System, I didn't include the older Civil Service Retirement System benefits in my comparison. The standard advice to a CSRS employee is to retire first and then look for a job in the private sector.)

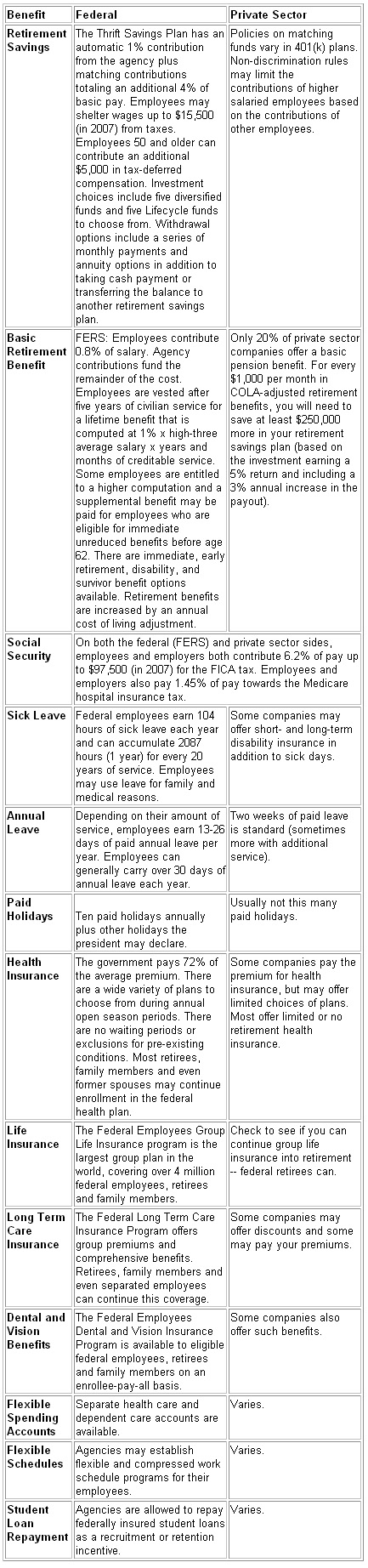

| Benefit | Federal | Private Sector | ||

| Retirement Savings |  | Policies on matching funds vary in 401(k) plans. Non-discrimination rules may limit the contributions of higher salaried employees based on the contributions of other employees. | ||

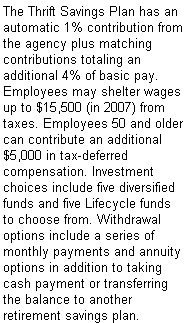

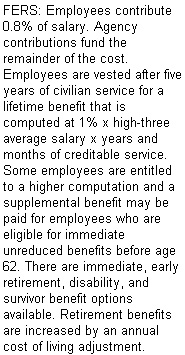

| Basic Retirement Benefit |

|

Only 20% of private sector companies offer a basic pension benefit. For every $1,000 per month in COLA-adjusted retirement benefits, you will need to save at least $250,000 more in your retirement savings plan (based on the investment earning a 5% return and including a 3% annual increase in the payout). | ||

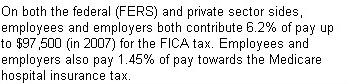

| Social Security |

|

|||

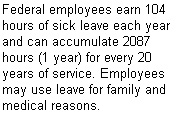

| Sick Leave |

|

Some companies may offer short- and long-term disability insurance in addition to sick days. | ||

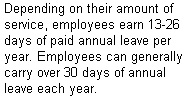

| Annual Leave |

|

Two weeks of paid leave is standard (sometimes more with additional service). | ||

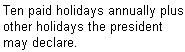

| Paid Holidays |

|

Usually not this many paid holidays. | ||

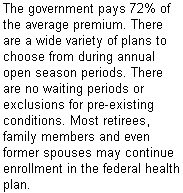

| Health Insurance |

|

Some companies pay the premium for health insurance, but may offer limited choices of plans. Most offer limited or no retirement health insurance. | ||

| Life Insurance |

|

Check to see if you can continue group life insurance into retirement -- federal retirees can. | ||

| Long Term Care Insurance |

|

Some companies may offer discounts and some may pay your premiums. | ||

| Dental and Vision Benefits |

|

Some companies also offer such benefits. | ||

| Flexible Spending Accounts |

|

Varies. | ||

| Flexible Schedules |

|

Varies. | ||

| Student Loan Repayment |

|

Varies. | ||

I'm self-employed, and I have to admit I'm glad I'm married to someone who works for the federal government. I share in all of my husband's insurance benefits, which is a big savings compared to having to enroll in an individual plan. We also have the security of lifetime coverage on both insurance and retirement benefits.

Finally, remember that there are some things that can't be measured by statistics - like the pride that comes with fighting crime and terrorism at the FBI or searching for cures for diseases at the National Institutes of Health. The deciding factor of continuing in your government career or heading for the private sector might have something to do with benefits, but it could also boil down to the feeling you get when you go to work every day.

Tammy Flanagan is the senior benefits director for the National Institute of Transition Planning Inc. , which conducts federal retirement planning workshops and seminars. She has spent 25 years helping federal employees take charge of their retirement by understanding their benefits.