This week, I want to introduce you to some new acronyms that you may need to understand if you are near age 65 or older and covered by one of the 156 plan choices that will be available in 2024. Open Season 2023 begins on Nov.13 and federal employees as well as retirees, survivor annuitants and eligible former spouses will be analyzing their options for the Federal Employees Health Benefits program and Federal Employees Dental and Vision Insurance Program as well as how much to set aside in a health care or dependent care FSA.

A new benefit is being automatically added to many of the FEHB program options for the 2024 plan year for retirees who are also enrolled in Medicare Part A and/or Part B: Medicare Part D, the prescription drug benefit under the government's national health insurance program. This benefit has been previously included in the Medicare Advantage options that have been added to many FEHB plans over the past few years and will also be available for some plans without the additional Medicare Advantage benefit. For plan year 2024, plans offering this benefit will automatically coordinate with FEHB through an Employer Group Waiver Plan. EGWPs are offered either as a standalone Prescription Drug Plan or a Medicare Advantage Prescription Drug plan.

You may find that if your plan is offering this benefit for 2024, they may provide separate brochures detailing these benefits which may have been mailed to you prior to open season. For example, BC/BS has published a brochure titled, "Get to know the FEP Medicare Prescription Drug Program." You can also find information on how your plan coordinates with Medicare on your plan websites. GEHA, like many FEHB plans, has a Medicare and a new Medicare Advantage link on their website where you will find explanations of the options that are available for members who want to add the Medicare Advantage option and for those who have Medicare A and B and prefer not to add the Medicare Advantage enhancement benefit. You can also learn more about how your FEHB plan coordinates with Medicare by checking Section 9 of the 2024 FEHB plan brochure.

It is not surprising that retirees have questions about these new benefits. Here are some that have come from members of the National Active and Retired Federal Employees Association over the past few weeks:

Q: Will the MA-PD or PDP have the same formulary as before or will it use a different formulary?

A: This is from Rick Tapnio, senior account manager for Aetna Federal Plans: Prescription drug benefits are improving in 2024 for members with Medicare. Eligible members will see lower copays and a lower limit on out-of-pocket costs with Aetna Medicare RX® offered by SilverScript®. The same drugs are covered but the formulary list is different. Therefore, some drugs could be covered under a different tier. However, it doesn't necessarily mean members will pay more because copays and coinsurance may be lower even if drugs move to a higher tier.

Q: Will the coverage be less restrictive with lower copays?

A: The greatest impact for members will be lower copays and less coinsurance coming out of their pocket.

Q: Which one of these two would someone use if covered under Aetna Direct as a retiree?

A: The PDP formularies will be on our website once they become available. Members can also connect with their plan's Member Services to research specific drugs thoroughly. After you reach your individual maximum out-of-pocket costs of $2,000, Aetna FEHB Plan will pay the rest of your annual drug costs.

Q: Am I correct in thinking that if I don't opt out of this drug enhancement I will be ineligible for drug coupons from manufacturers because I will have drug benefits from Medicare?

A: In general, most manufacturer's discount programs exclude those who are enrolled in a Part D program. To know for sure, you must check the eligibility requirements for the copay card/program. Below is a sample of the wording for one of the cards that is often asked about: Eliquis. Enrollment in the enhanced Medicare Prescription Drug Program (MA-PD or PDP) is a Part D plan and a member would not meet the requirements for eligibility for this copay card. However, members enrolled in MA-PD or PDP can get a 90 day supply of Eliquis for a very low rate.

ELIQUIS copay card has the following eligibility requirements:

You are insured by commercial insurance and your prescription insurance coverage does not cover the full cost of your prescription, that is, you have a co-pay obligation for ELIQUIS;

You do not have prescription insurance coverage through a state or federal healthcare program, including but not limited to Medicare Part D, Medicaid, Medigap, Veterans Affairs Department or Defense Department programs; patients who move from commercial plans to state or federal healthcare programs will no longer be eligible;

You are 18 years of age or older; and

You are a resident of the United States, Puerto Rico, or other select U.S. Territory.

Q: Does the out-of-pocket expense ceiling under the Medicare PDP enhancement take into account my out of pocket expenses incurred under my overall FEHB Plan catastrophic spending cap AND those incurred under the new Medicare PDP?

A: If you are enrolled in both Parts A and B of Medicare, there should be no, or very little, out-of-pocket medical expenses incurred as many plans (but not all) will waive your deductible, copays and coinsurance for both inpatient and outpatient medical services (not pharmacy) when Medicare A and/or B are the primary payer. The only way to reach the catastrophic out-of-pocket maximum with your FEHB plan when you have Medicare A and B as primary payer (with plans that wrap around Medicare by waiving your cost-sharing including deductible, copays and coinsurance) is by having extremely large prescription drug expenses. One of the benefits of the MA-PD and PDPs is a lower cap on out-of-pocket prescription drug expenses. If you don't enroll in Part B of Medicare, you will be required to pay cost-sharing for outpatient care which can add up to a much higher catastrophic cap on your out-of-pocket costs. See Section 4 of your plan brochure, Your Cost for Covered Services and also Section 9 of your plan brochure, Coordinating Benefits with Medicare and Other Coverage.

For example, according to Jennifer Vendur, account manager for the federal employee BC/BS Program, BC/BS Standard option will have a $2,000 Rx out-of-pocket max for 2024 and for Basic Option there will be a $3,250 Rx out-of-pocket max. Using Standard option self-only numbers as an example: The overall BC/BS Standard Option out-of-pocket maximum is $6,000. The PDP has a limit within that $6,000 that says you don't have to pay more than $2,000 toward prescription drugs. The $2,000 is part of the $6,000 – not in addition to it. If you have Medicare A and B as your primary coverage, regardless of your prescription drug copays, you would not spend more than $2,000 out-of-pocket in 2024 since your inpatient and outpatient medical cost-sharing is waived when Medicare is the primary payer. Every time you pay a copay or coinsurance (%) for a prescription on the PDP, this counts toward the Rx out-of-pocket max. Once you hit the $2,000 max, you don't pay any more Rx copays or coinsurance for the remainder of the calendar year. These amounts also count toward the overall out-of-pocket maximum of $6,000. The only people who will continue to pay medical copays are those without both parts of Original Medicare (A and B). If you opt out of PDP, your prescription drugs still count toward your out-of-pocket max, you just don't get the $2,000 Rx cap – everything applies to the $6,000 out-of-pocket max, just like it does now.

Vendur further explained that under the BC/BS PDP, the formularies are expanded. They include all Medicare Part D drugs PLUS everything on the traditional formulary for that plan. For example, if a drug is on the traditional formulary for Standard Option, it will also be on the PDP Standard Option formulary. If the drug is on the traditional formulary for Basic Option, it will also be on the PDP Basic option formulary. However, just like now, the Standard Option prescription drug formulary is different from the Basic Option formulary.

Here are some benefits under the Inflation Reduction Act of 2022 that apply to MA-PDs and PDPs available in many FEHB plans for 2024:

You will not pay a separate premium for your prescription drug coverage although some higher income participants may need to pay a Part D Income-Related Monthly Adjustment Amount (IRMAA). If your income is above a certain limit (in 2024, above $103,000 if you file individually or $206,000 if you're married and file jointly), you'll pay an extra amount in addition to your plan premium (sometimes called "Part D-IRMAA"). If you are subject to the Part D IRMAA surcharge, you are permitted to opt-out of the PDP and MA-PD, but doing so will result in a loss of the other benefits of this coverage.

Beginning in 2023, Part D enrollees will pay no more than $35 per month for covered insulin products in all Part D plans.

Here are some additional things to know about these new benefits designed to make prescription drugs more affordable:

If you or someone you know struggles to pay for their healthcare expenses, there is Extra Help (sometimes called Low Income Subsidy or LIS) that Medicare offers to people with low incomes and limited assets. If you qualify, you'll get help with drug costs that Medicare doesn't cover including your plan premium, drug deductible and prescription copays. Depending on your income and resources, you could save an average of $5,000 per year. Less than half of the people eligible for Extra Help sign up.

If you decide you no longer wish to be enrolled in the PDP or MA-PD, you may contact your FEHB plan to cancel your enrollment at any time. You may re enroll during a subsequent open season period.

The PDP plans have automatic enrollment, so the only thing you may need to do if you don't want this coverage is to opt-out. However, if you are interested in a MA-PD option under one of the many FEHB plans offering this Part C / Medicare Advantage benefit, you will need to "opt-in" to receive these benefits. Contact your FEHB plan for additional information.

Remember, Open Season will run from Nov. 13 to Dec. 11, 2023.

Federal annuitants will have higher healthcare costs in 2024. The enrollee share for Federal Employees Health Benefits Program premiums is rising 7.7%, and the standard Medicare Part B premium is increasing 5.9%, or $9.80, to $174.70/month.

Medicare Part D reforms that passed in 2022 are being implemented and offer annuitants an opportunity to save money next year in two ways—lower out-of-pocket prescription drug costs and protection against high out-of-pocket prescription drug costs.

We'll discuss Part D reform and the two plan options available to annuitants next year—Part D Prescription Drug Plans and FEHB Medicare Advantage Plans.

Part D Reform

The Inflation Reduction Act of 2022 contained major Part D reforms, and some have already been adopted. This year, Part D plans began offering insulin at no more than $35/month. In 2024, there will no longer be any enrollee cost share over the catastrophic coverage limit, and Part D premiums are not allowed to increase more than 6% per year. In 2025, Part D plans will have a $2,000 out-of-pocket spending cap.

Earlier this year, the Office of Personnel Management encouraged FEHB plans to offer more Part D options so that federal annuitants could benefit from improved prescription drug coverage. In a letter to FEHB carriers, OPM offered two ways for FEHB plans to provide Part D coverage—Part D Prescription Drug Plans, which had never been offered to annuitants before, and FEHB Medicare Advantage Plans, which have been available over the last few years.

New Part D Prescription Drug Plans

The following 17 FEHB plans will offer a Part D Prescription Drug Plan next year, with no additional premium:

To receive OPM approval, the PDP must provide as good or better prescription drug benefits than the FEHB plan, at no additional cost. After our review of the 2024 PDP benefits, we concur with OPM's assessment. The PDP benefits are as advertised and are at least as good as the FEHB prescription benefits, in some cases with even lower out-of-pocket prescription drug costs. This is especially true for the PDPs, marked above, that provide the $2,000 prescription drug maximum out-of-pocket, a year earlier than what is required by law. Annuitants with moderate to high prescription drug costs will benefit greatly from enrolling in one of those plans next year.

If you are a member of an FEHB plan offering a PDP and are enrolled in either Medicare Part A or Medicare Parts A & B, you'll be auto-enrolled in the PDP plan for prescription drug coverage. BCBS plans are the exception to the rule; they will only auto-enroll when you have both Parts A & B. Your plan will send you written notification of the auto-enrollment, and you'll have 30 days to opt out of the PDP. After the 30 days, you'll receive a new prescription drug insurance card, and your Part D coverage will begin 1/1/2024.

If you aren't in one of the 17 FEHB plans that offer a PDP and are interested in enrolling, you can visit the website of a plan offering a PDP to find enrollment instructions. Most plans will have an online and telephone enrollment option.

Annuitants filing individually with income above $103,000, or filing jointly with income above $206,000, will be subject to an Income Related Monthly Adjustment Amount with Part D enrollment. Keep in mind that Part D IRMAA is far less than Part B IRMAA: The first income tier is $12.90/month per person compared to Part B IRMAA which is $69.90/per month per person. With lower out-of-pocket prescription drug costs and catastrophic protections in some plans, the PDP benefits will outweigh IRMAA for many annuitants.

If you decide to opt out of PDP coverage because of IRMAA or any other reason, you can enroll into a PDP in the future, without penalty, as FEHB prescription drug is considered creditable coverage by OPM.

Make sure to check that any existing prescription drugs will remain covered in the PDP. This drug formulary is managed by CMS, not OPM, and there could be differences in how they're classified in the PDP compared to the FEHB plan. The official FEHB plan brochure of the 17 plans offering a PDP will discuss coverage either in Section 9 or Section 5(f). Most of the plan websites have additional information including a formulary lookup and pharmacy pricing tool.

FEHB Medicare Advantage Plans

MA plans, or Medicare Part C, package original Medicare with a Part D plan. These plans have been around for the last few years, and there are even more MA plans available to annuitants next year.

National plans offering an MA plan: GEHA High & Standard (new for 2024), NALC High, MHBP Standard, APWU High, Rural Carrier, Foreign Service, SAMBA High & Standard, Compass Rose High, and Aetna Advantage.

Local plans offering an MA plan: United Healthcare, Kaiser, MDIPA, CDPHP, Health Alliance HMO (new for 2024), Healthnet of California, and UPMC Standard.

Many of the MA plans offer a Part B premium reimbursement ranging between $75 to $150 per month. However, there are some Kaiser plans that will reimburse up to $250/month for individuals that pay a higher Part B premium because of IRMAA or a late enrollment penalty.

Also, many, but not all, of the MA plans have $0 out-of-pocket costs for approved healthcare services from providers that accept Medicare and the plan, besides prescription drugs. You can also find special benefits from some of the MA plans such as a gym membership through Silver Sneakers, hearing aid coverage, dental care, and a quarterly over-the-counter pharmacy item allowance.

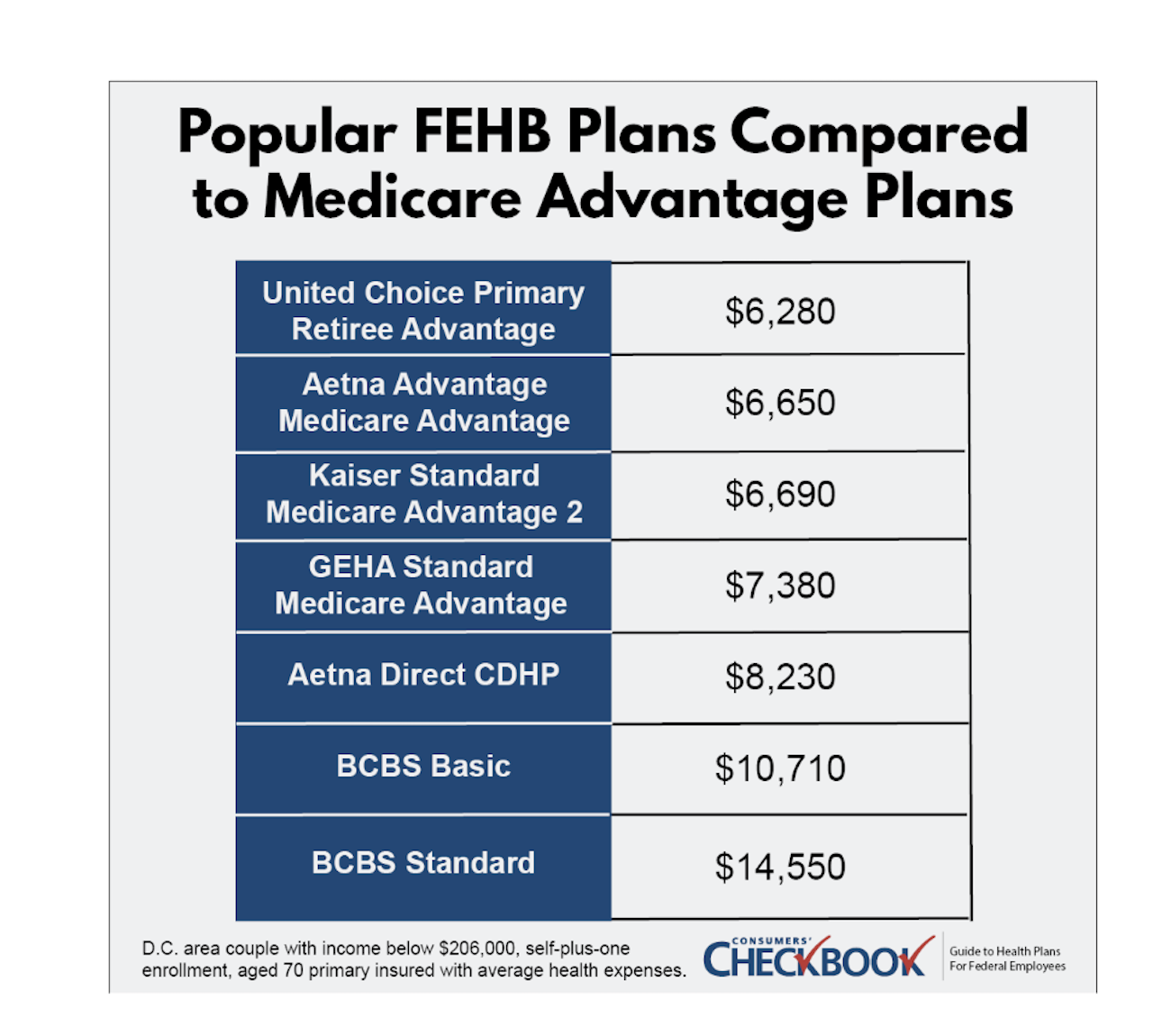

The combination of a significant reduction in Part B premiums plus $0 out-of-pocket healthcare costs outside of prescription drugs provides annuitants massive healthcare savings. For every FEHB and FEHB MA plan, Checkbook's Guide to Health Plans for Federal Employees provides a yearly cost estimate, which is a combination of the for-sure expense of premium (both FEHB and Part B in this case) and the likely out-of-pocket costs you'll face based on age, family size, and expected healthcare usage.

A D.C.-area couple with a 70-year-old primary insured, average healthcare expenses, income below $206,000, and self-plus-one enrollment could save $8,270 next year in likely healthcare expenses switching from BCBS Standard to United Choice Primary Retiree Advantage.

You must have Medicare Parts A & B to enroll in an FEHB MA Plan. To sign up, first enroll with OPM in the corresponding FEHB plan and wait a business day or two for OPM to update the plan with a new member roster. The final step is enrolling in the MA plan, which must be done directly with the plan either through its website or through a special MA enrollment phone number. To find out more information about the MA plan benefits, go to section 9 of the official FEHB plan brochure or to the plan website.

While an FEHB MA plan will be the least costly choice for most federal annuitants, it might not be the best option for everyone. If you have Part B but pay more than the standard Part B premium, through IRMAA or a late enrollment penalty, the higher Part B premium will erode the financial value that the MA plans provide. However, if you are only in the first tier of IRMAA, the Part B reimbursement and zero cost share besides prescription drugs will likely still result in MA plans as the cheapest plan choice.

If you spend considerable time abroad, most of the FEHB MA plans will not cover routine care overseas. Only UnitedHealthcare has some routine overseas coverage.

Pay attention to the FEHB MA plan's provider network. The plans state that you can see any provider that accepts Medicare, but the provider must also accept the plan. Make sure to check the FEHB MA online provider directory to see that both your existing providers and any providers you might want to see in the future will be covered.

The Final Word

Federal annuitants will face greater healthcare costs in 2024, with both higher FEHB and Medicare Part B premiums. For annuitants that face moderate to high prescription drug costs, new Part D prescription drug coverage will be an important way to save money next year.

This upcoming Open Season will be one of the most important in recent years for annuitants to evaluate their existing plan against those that offer Part D coverage. If your current FEHB plan doesn't have new Part D coverage, you'll want to review those with a PDP to see if one would be a better fit than your existing plan.

FEHB MA plans offer federal annuitants an opportunity to save some serious money on all your healthcare costs, not just prescription drugs. How much you'll save depends on your current FEHB plan and which FEHB MA plan you choose to enroll in for next year.

Kevin Moss is a senior editor with Consumers' Checkbook. Checkbook's 2024 Guide to Health Plans for Federal Employees will be available on the first day of Open Season, Nov. 13. Check here to see if your agency provides free access. The Guide is also available for purchase and Government Executive readers can save 20% by entering promo code GOVEXEC at checkout.

This open season, make a plan to secure your family’s financial future with Group Term Life Insurance from WAEPA. Feds can replace or supplement any existing coverage you may have, with up to $1.5 million in protection. See why more than 50,000 Feds and their families choose WAEPA to be there for life’s biggest moments.

Before Open Season begins on Nov. 13, it's important to review what's new in the Federal Employees Health Benefit Program. As in previous years, there are significant premium, benefit, and plan availability changes that will affect both active and retired federal employees. We'll walk you through important updates impacting your budget and plan choice in 2024.

The Plans

With Humana exiting the FEHB market, there are far fewer plans available in 2024 than 2023―only 156 compared to 271. Besides Humana, additional HMO plans are no longer participating next year, including UnitedHealthcare Choice Plus Advanced in Florida and Georgia, United HDHP in Iowa and Kentucky, Indiana University Health Plan, AultCare in Ohio, and Aetna Open Access in Kansas and Missouri. Remember: If your plan is no longer available next year, you must choose a new one or you will be auto-enrolled in the least expensive national PPO plan, GEHA Elevate.

Besides plans leaving, service area changes could impact your choice of available plans. Kaiser Permanente in Colorado is both adding and removing counties for High, Standard, and Prosper plans; Blue Shield of California High Open Access is dropping counties; and Capital Health Plan in Florida, Health Alliance in Michigan, and HealthPartners in South Dakota are all adding counties.

There aren't many new plan options for 2024. Compass Rose has changed their offerings with both a high and standard option. They have also expanded their enrollment criteria by granting Veterans Affairs Department employees and retirees with eligibility. Sentara High has a new plan available in Northern Virginia.

The Benefits

Every federal employee and annuitant should check Section 2, "What's New for 2024," of their current plan's official FEHB brochure, plus any other plan they're considering. This is where the plan will inform you of important benefit changes. While some plans will have very few and may only mention premium, other plans may have very different benefits in 2024 that could affect your decision.

For example, United Choice Plus Advanced is increasing the catastrophic out-of-pocket maximum from $3,000 to $6,000 for self-only enrollees and from $6,000 to $12,000 for self-plus-one and self-&-family enrollees.

Plans are offering some new benefits next year. MHBP plans have enhanced maternity programs as a wellness benefit, SAMBA plans are offering doula coverage, BCBS plans have both marital and family counseling and medically necessary genetic testing.

Improved Fertility Coverage

This is by far the biggest FEHB benefit change. OPM mandated that all FEHB plans in 2024 must provide coverage of artificial insemination procedures and IVF-related fertility drugs. Families that need these services will still face high out-of-pocket costs, however, as the cost share is sometimes as much as a 50% coinsurance. Also, some plans, like Aetna Advantage, don't count out-of-pocket costs for fertility services toward the out-of-pocket maximum.

The fertility coverage available to you is somewhat determined by where you live. FEHB plans based in Hawaii, HMSA & Kaiser, have covered IVF for many years because of laws passed in that state. And, historically, IVF coverage has been more widely available in HMO plans.

Next year you can find IVF coverage in the following HMO plans:

Presbyterian High, Standard, and Wellness in NM

UPMC HDHP and Standard in PA

Calvo's Selectcare in Guam

Triple S Salud in Puerto Rico

SelectHealth HDHP and High in UT

Baylor Scott & White Basic and Standard in TX

Health Alliance HMO in IA/IN/IL

Priority Health High, Standard, and Value in MI

Two restricted enrollment PPO plans offer improved IVF coverage in 2024: Rural Carrier and Foreign Service.

And, importantly, one national PPO plan with open enrollment has gone above and beyond the OPM mandate. BCBS Standard now has a $25,000 annual maximum for assisted reproductive technologies . Artificial insemination procedures and fertility drugs do not count toward the $25,000 annual maximum. Do keep in mind though that BCBS Standard has the highest premium of any national PPO plan.

Higher Premiums

Overall, the average enrollee share of premium is rising 7.7% in 2024. This is slightly below last year, which was an 8.7% increase. When combined, however, this two-year span is one of the highest periods of increased premiums FEHB enrollees have faced in recent history.

Higher Contribution Limits for Tax Preferred Savings Accounts

With higher premiums and the potential for higher out-of-pocket healthcare costs in 2024, it's essential that active federal employees maximize the opportunity to save by using tax-preferred savings accounts.

Health Savings Accounts are available from High-Deductible Health Plans. HDHPs contribute a portion of the premium into the HSA as a monthly premium pass through. The total amount contributed to the HSA varies by plan, but ranges from $900 to $1,200 for self-only enrollees and $1,800 to $2,400 for self-plus-one and self-&-family enrollees. In 2024, the HSA contribution limit from the FEHB plan and employee is increasing to $4,150 for self-only enrollees and $8,300 for self-plus-one and self-&-family enrollees.

Only about 20% of all federal employees use a Flexible Spending Accounts (FSA), which is a great way to save about a third of the cost on a qualified healthcare expense. FSA contribution limits for 2024 have not been released by the IRS, but the limit is expected to rise to $3,200.

Improved Prescription Drug Coverage for Annuitants

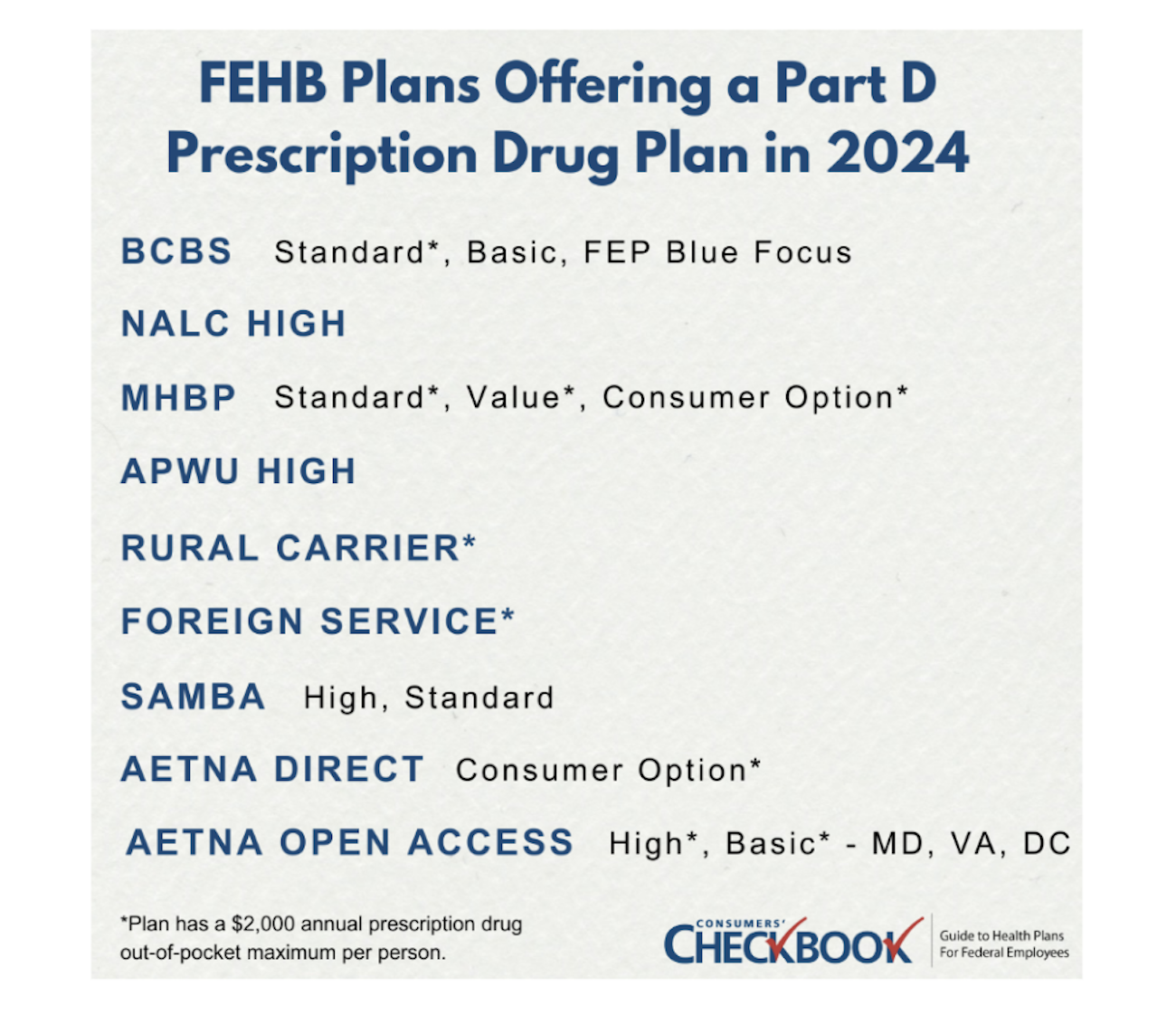

There are 17 FEHB plans that will offer a new Part D prescription drug plan in 2024. Plan members that have Medicare Part A or Medicare Parts A & B will be auto-enrolled in the Part D plan, except for BCBS plans which will only auto-enroll members that have both A & B.

BCBS Basic, Standard, FEP Blue Focus

NALC High

MHBP Standard, Value, Consumer Option

APWU High

Rural Carrier High

Foreign Service High

SAMBA Standard, High

HealthPartners Standard, High

Aetna Direct Consumer Option

Aetna Open Access Basic High – DC, MD, VA

Impacted members will receive communication of the new Part D coverage from their insurance plan and will have the opportunity to opt-out if they wish. However, almost everyone should keep the new Part D coverage. Why? Because the Part D prescription drug coverage is as good or better than what's available in the FEHB plan, at no extra premium. Additionally, BCBS Standard, Rural Carrier High, Foreign Service, and the MHBP and Aetna plans have all added a $2,000 prescription drug out-of-pocket max, which could have a major impact on annuitants that face moderate to high prescription drug expenses.

High income annuitants will be subject to an Income Related Monthly Adjustment Amount (IRMAA) for Part D coverage. However, the Part D IRMAA is much lower than for Part B. For the first tier of IRMAA, individuals with yearly income above $103,000 but less than $129,000 and couples with income above $206,000 and below $258,000, you'll pay an extra $12.90/month for Part D compared to an extra $69.90/month for Part B. The enhanced Part D benefits will outweigh Part D IRMAA for most.

The Final Word

Your FEHB plan will change for 2024. Most will see increased premiums next year, and some 2023 FEHB plans won't be available in the new year. There could be an important benefit that you use that has a new pre-authorization requirement, or there could be a newly available benefit next year. Make sure you review Section 2 of the official plan brochure to see how your plan is changing.

Federal employees and annuitants will both face higher healthcare costs in 2024. Active employees have access to tax-preferred savings accounts while working, but many don't take advantage of this easy way to save on qualified healthcare expenses.

Annuitants will face both higher FEHB plan premiums and a higher Medicare Part B premium. However, new Part D prescription drug coverage available from certain FEHB plans will be an important way for annuitants that face moderate to high prescription drug costs to save money.

Kevin Moss is a senior editor with Consumers' Checkbook. Checkbook's 2024 Guide to Health Plans for Federal Employees will be available on the first day of Open Season, November 13th. Check here to see if your agency provides free access. The Guide is also available for purchase and Government Executive readers can save 20% by entering promo code GOVEXEC at checkout.

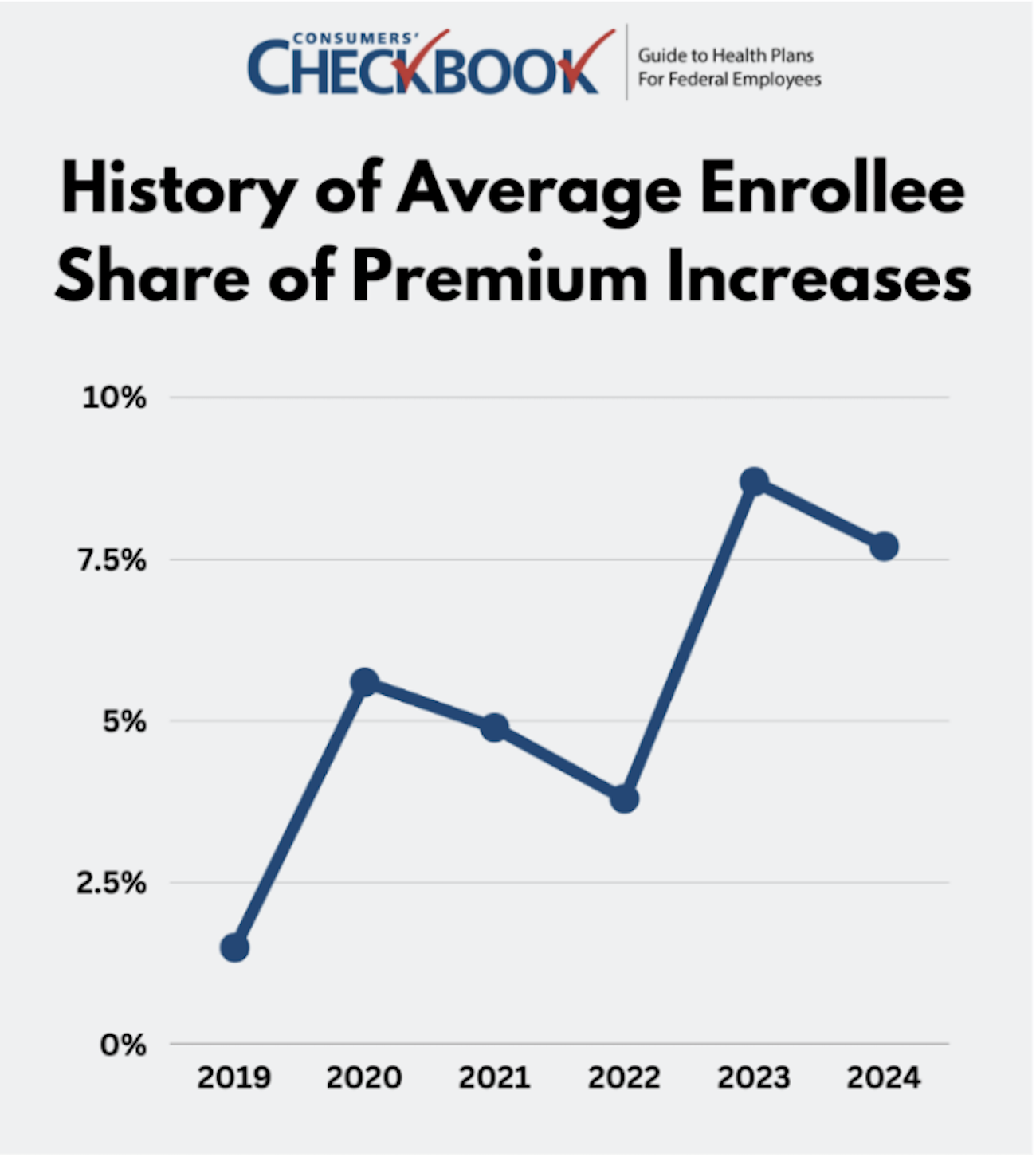

Last week, OPM released the first batch of information for the 2024 Federal Employee Health Benefits Open Season. Federal employees and annuitants will, on average, pay 7.7% more in FEHB premiums next year. OPM cites increased cost and use of prescription drugs, emergency room care, and outpatient care as the primary reasons for the increase in premiums.

How will higher premiums impact your FEHB plan choice for the upcoming open season? We'll walk you through changes in popular plans, discuss which ones saw their premiums increase above and below the average, provide enrollment advice for two-person families, and discuss FEDVIP dental and vision plan premium changes.

Recent History of FEHB Premium Increases

Next years 7.7% premium increase is less than the 8.7% increase of 2023, but it's still much higher than previous years. In 2022, the average enrollee increase was only 3.8%. While no one can predict the future, federal employees and annuitants should prepare to pay higher premiums and a higher rate of increase going forward.

How Premiums are Changing in 2024

While the average enrollee share of premium is going up 7.7%, not all plans reflect that trend. For the 156 FEHB plans available in 2023 and 2024, premiums will decrease in 28 plans, stay the same in 15 plans, increase below the 7.7% average in 64 plans, and increase above the 7.7% average in 49 plans.

Some of the changes are striking. For example, the largest decrease in enrollee share of premium is from the Baylor Scott & White Standard Health Plan (A8), available in Central Texas, which costs 54% less in 2024, saving self-only enrollees around $1,500 next year. Aetna Advantage, a national PPO plan, has the same premium in 2024 as 2023. The largest increase in enrollee share of premium is from Kaiser Permanente High (F8) in the Atlanta region, which is 22% more in 2024 and will cost self-only enrollees around $1,100 more next year.

How is your plan's premium changing next year? Even if you're happy with your existing FEHB plan, it will most likely be more expensive in 2024. Not all premiums rose at the same rate, and there may be new plan bargains available to you, which is why it's important to know how this for-sure expense will impact your budget in 2024.

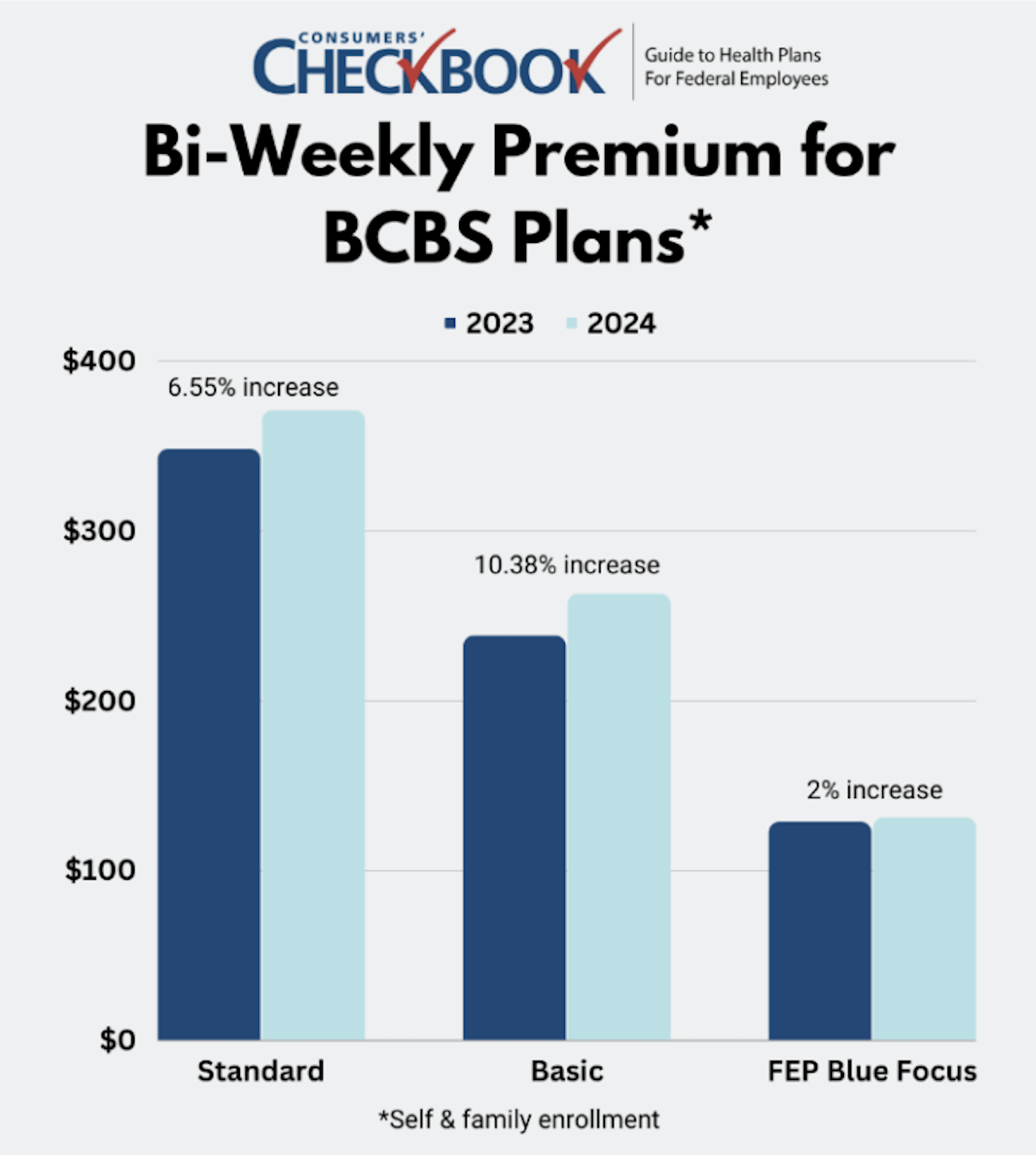

Blue Cross Blue Shield

Almost two-thirds of federal employees are enrolled in one of the Blue Cross Blue Shield plans—Standard, Basic, or FEP Blue Focus. How did the BCBS plan premiums change?

Basic increased above the all-plan average, Standard increased just below the average, and FEP Blue Focus increased well below the average.

This upcoming Open Season is a good opportunity to assess whether your current plan is still the best fit for your needs. For Basic and Standard plan members, are you enrolled in the right BCBS plan? Now might be the opportunity for you to save one or two thousand dollars a year in premium by switching to FEP Blue Focus.

Of course, there are many differences between the Standard, Basic, and FEP Blue Focus plans, but three of the most important are Standard is the only one where:

You can see out-of-network providers,

Receive mail-order prescription drugs (Basic has mail-order prescription drug coverage only for annuitants with Part B),

And receive fertility coverage, including assisted reproductive technology (ART) coverage up to $25,000 annually (a new benefit for 2024).

If you're enrolled in Standard and don't use those benefits, you'll save money switching to Basic or FEP Blue Focus and you'll get to keep your existing BCBS in-network providers.

Self-Plus-One vs Self & Family Enrollment

Married couples and two-person families can enroll as self-plus-one or self-and-family. Most of the time, self-plus-one is the cheaper enrollment choice, but not always. In 2024, there are 49 FEHB plans where self-&-family enrollment is less expensive than self-plus-one, and 11 plans where the premiums are the same.

There is a sizable amount of money at stake that you could save, or waste, based on your enrollment decision. For example, a two-person family considering the D.C.-area Kaiser High (E3) plan can save $59.68 bi-weekly enrolling as self-&-family compared to self-plus-one. That adds up to $1,552 annually.

You can find premiums by enrollment type on the last page of any FEHB brochure (found on the OPM plan comparison tool and Checkbook's Guide to Health Plans) once they are released in November, just before the start of Open Season. Look for the enrollee share of premium and choose the enrollment option that is cheaper. You receive the same plan benefits regardless of enrollment type.

FEDVIP Premiums

FEDVIP premiums have historically increased at a much lower rate compared to FEHB plans. For 2024, FEDVIP dental plan premiums will increase 1.4% on average and FEDVIP vision plan premiums will increase by 1.1%.

The Final Word

Your FEHB premium will most likely go up in 2024, and possibly by quite a bit. The 7.7% increase is only an average, and many plans will cost more. While only one factor in your overall plan selection decision, the premium is important because it's a for-sure expense. You absolutely must check to see how yours is changing for 2024 and consider whether another plan is a better value for you and your family. The 2024 FEHB Open Season starts Nov. 13 and ends Dec. 11.

Kevin Moss is a senior editor with Consumers' Checkbook. Checkbook's 2024 Guide to Health Plans for Federal Employees will be available on the first day of Open Season, Nov.13. Check here to see if your agency provides free access. The Guide is also available for purchase and Government Executive readers can save 20% by entering promo code GOVEXEC at checkout.

Federal employees and retirees will pay an average of 7.7% more on their health care premiums in 2024, a slight decrease from last year's biggest price hike in a decade.

The government's share of Federal Employees Health Benefits Program premiums will increase by an average of 5%, bringing the overall increase to 5.8%, according to the Office of Personnel Management. In 2023, feds were estimated to pay an average of 8.7% more on premiums than the previous year, and the overall average premium increase of 7.2% was the highest for the nation's largest health insurance program since 2011.

On average, federal workers enrolled in "self-only" plans will pay an additional $8.05 per biweekly pay period, while feds in "self plus one" insurance plans will pay $16.73 more next year. Federal employees enrolled in family coverage will pay an average of $21.16 per pay period in 2024.

Under the Federal Employees Dental and Vision Insurance Program, the average premium for dental plans will increase by 1.4%, while premiums for vision coverage will increase by an average of 1.1%.

The FEHBP's annual open season, in which federal employees can choose from a variety of national and regional insurance carriers and coverage plans, will run from Nov. 13 to Dec. 11. More federal workers will be required to select a new plan than usual this year, as the overall number of options will reduce from 271 plan choices to 159. That's because Humana is withdrawing both from the FEHBP and from employer-sponsored insurance as a whole over the next two years.

Beginning next year, OPM has secured additional benefits for FEHBP enrollees in the form of "comprehensive" coverage of FDA-approved anti-obesity medication and improved access to mental health and substance abuse disorder services, including telehealth, at low or no cost sharing. Additionally, the program will provide stronger coverage of treatments related to assisted reproductive technology like artificial insemination, as well as gender-affirming care for transgender and other gender diverse enrollees.

And insurers will expand coverage of prenatal and postpartum care, including childbirth education classes, group prenatal care, as well as home-based health care services both during pregnancies and postpartum.

Additionally, OPM announced that it is expanding eligibility for Dependent Care Flexible Spending Accounts to active-duty members of the military and active guard reserve members and their 400,000 dependent family members.

High Deductible Health Plans , which include Health Savings Accounts , are one of the cheapest health plan options available to federal employees. With an increase in HSA contributions for plan year 2024, HDHPs will offer additional value going forward. If you haven't considered an HDHP in the past, now is a good time to review whether it could help you save money on your current and future healthcare expenses or be an additional stream of income in retirement.

HDHP and HSA Basics

HDHPs encourage enrollees to be mindful healthcare consumers by having a high deductible in place. Here's how it works: Before the deductible, you'll pay the full amount allowed by the plan for health services. After the deductible, you'll generally pay a percentage of billed expenses, or coinsurance, that varies by plan and typically ranges between 5% to 20%. In some cases, depending on the health service, it can be higher.

To help you out before the deductible is met, all HDHPs provide free in-network preventive care including annual physicals, well-child visits, mammograms, and immunizations.

Additionally, all FEHB HDHPs fund an HSA that you can use to pay for out-of-pocket expenses. The plan-funded amount ranges between $750 to $1,200 for self-only enrollments and from $1,500 to $2,400 for self-plus-one and self-and-family enrollments. Plan contributions to the HSA are deposited monthly.

You can also make voluntary contributions to an HSA that are triple tax advantaged—they go in tax-free (either as a pre-tax payroll deduction or as a deduction when you file your taxes if you make a lump-sum contribution), grow tax-free, and exit tax-free if used for qualified healthcare expenses.

The HSA is managed by a financial services company, and you'll be able to choose how to invest your funds with investment options similar to an Individual Retirement Account (IRA) with greater choice than what is available through a Thrift Savings Plan. Any unused funds will roll over to the following year, and there is no roll-over cap. Your HSA is owned by you, the enrollee, which means it's fully portable if you leave federal service or switch FEHB plans.

How Much Can You Save Switching Plans?

Depending on your current FEHB plan, you could save thousands of dollars by switching to an HDHP. Keep in mind that HDHPs tend to have lower premiums than many popular non-HDHPs and have the added benefit of plan HSA contributions.

Checkbook's Guide to Health Plans ranks all FEHB plans based on a total cost estimate that's a combination of for-sure expense (premium) plus likely out-of-pocket costs you'll face based on age, family size, and expected healthcare usage.

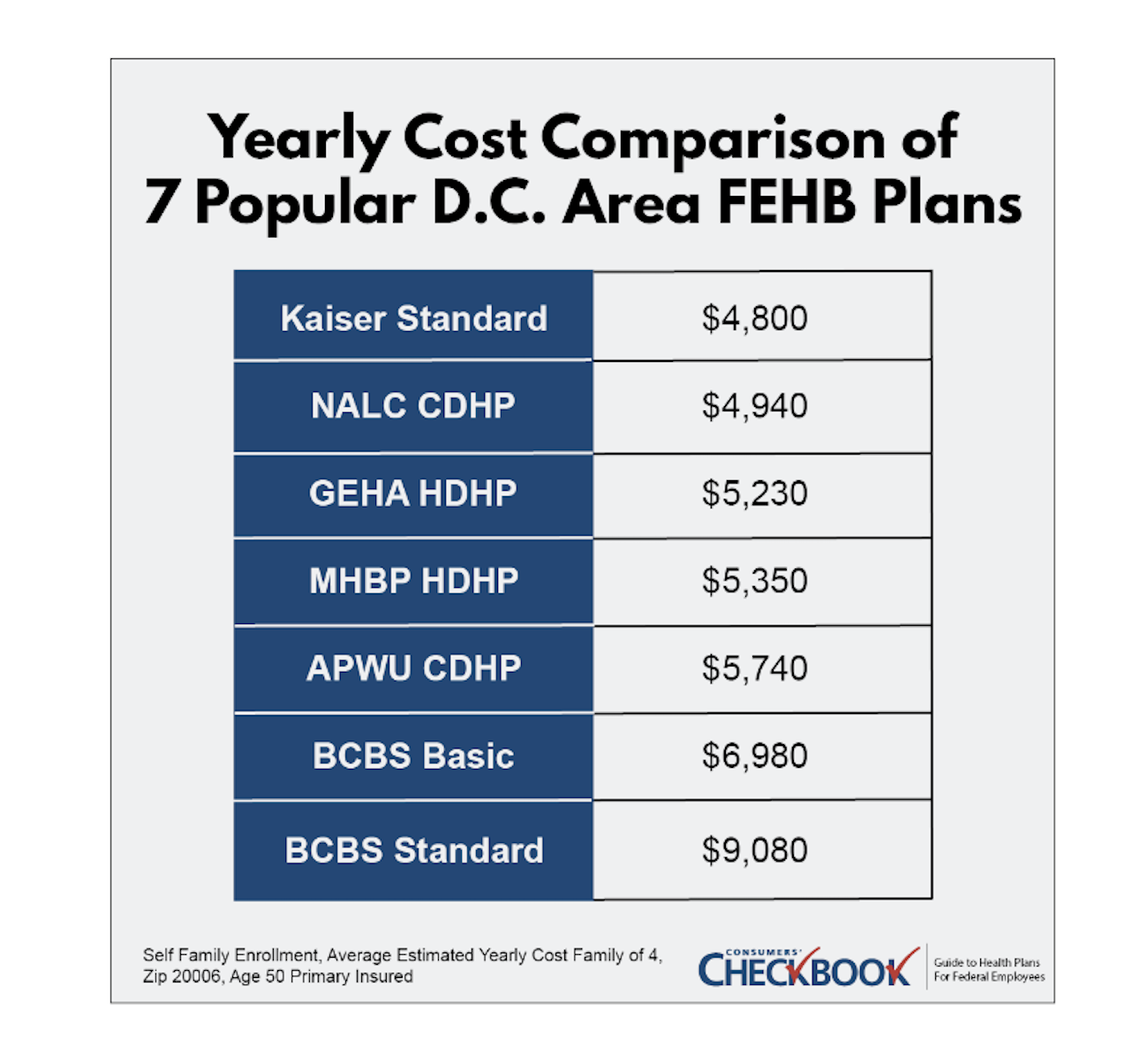

For 2023 coverage, we calculate that a Washington, D.C.-area family of four could have saved $3,850 in estimated total costs this year by switching from BCBS Standard to GEHA HDHP, or $1,750 in estimated total costs by switching from BCBS Basic to GEHA HDHP.

Retirement Super Weapon

As you approach retirement, you have an opportunity to contribute even more to your HSA. Once you turn 55, you'll be able to contribute an additional $1,000 per year as a "catch-up" contribution on top of the normal contribution maximum.

Once you turn 65, a big change with your HSA takes place: You're allowed to make non-medical distributions and only pay your regular tax obligations. Prior to age 65, non-medical distributions would create a 20% income-tax penalty on top of your normal taxes. This change gives you more flexibility on how to use your HSA funds, including as supplemental retirement income.

There are other healthcare-related qualified expenses that you can choose to use your HSA for in retirement and pay no taxes on. The premium for long-term care insurance, which pays for nursing homes and assisted living centers, is a qualified expense, as are Medicare Part B and D premiums both for you and a spouse.

What's New For 2024

In May, the IRS announced higher HSA contribution limits for plan year 2024. For self-only enrollments, the combined HSA contribution between enrollee and plan will increase by $300 from $3,850 to $4,150. Self-plus-one and self-and-family enrollments will see HSA contributions rise $550 from $7,750 to $8,300.

Additionally, the minimum HDHP deductible will rise slightly next year to $1,600 for self-only enrollments and $3,200 for self-plus-one and self-and-family enrollments. Also, the maximum out-of-pocket expense (deductible, copayments, coinsurance, not premiums) will increase to $8,050 for self-only enrollments and $16,100 for self-plus-one and self-and-family enrollments. Finally, HSA catch-up contributions are unchanged in 2024 and remain $1,000.

Reasons to Not Join an HDHP

While an HDHP with an HSA will be the cheapest plan option for many, it may not be the best choice for all.

If you have an accident or unplanned hospitalization at the start of a plan year, you would be responsible for paying the entire deductible and possibly a portion of expenses above the deductible depending upon the service's cost. This event could produce an unexpected health bill of a few thousand dollars. If that would cause financial distress, you would be better served with a non-HDHP that has either no deductible or a low deductible with fixed co-pays for healthcare services.

Additionally, any employees that have significant prescription drug expenses will probably be better served by a non-HDHP. You'll be paying the allowed charge for most prescription drugs before you reach the deductible in an HDHP. A non-HDHP that covers your prescription and that has a fixed co-pay will be less expensive for most.

The Final Word

For most federal employees, an HDHP will be the least costly plan option available especially when considered as a long-term option. If you're able to preserve the plan contribution and make additional contributions into the account, the HSA can grow very fast. We've heard from many federal employees that have HSAs with a balance of $50,000 or more because they've been enrolled in an HDHP for many years and have contributed the max every year. And, when you turn 65, the HSA becomes a multi-purpose super weapon that can either help pay for almost every healthcare expense you'll face or be used as an extra source of income.

However, federal employees are on borrowed time to maximize an HSA's tax-preferred benefits. Once you retire and are on Medicare, you no longer qualify to receive an HSA from an HDHP and you can no longer make voluntary contributions to your HSA.

With increased contribution limits, you'll be able to sock away even more money into an HSA next year. Give HDHPs a look this fall during Open Season to see if this plan type can help you save money now and in the future.

Kevin Moss is a senior editor with Consumers' Checkbook. Checkbook's Guide to Health Plans for Federal Employees is available to many federal employees for free; check here to see if your agency provides access. The Guide is also available for purchase and GovExec readers can save 20% by entering promo code GovExec at checkout.

This open season, make a plan to secure your family’s financial future with Group Term Life Insurance from WAEPA. Feds can replace or supplement any existing coverage you may have, with up to $1.5 million in protection. See why more than 50,000 Feds and their families choose WAEPA to be there for life’s biggest moments.

This message was sent from Government Executive to {email}. You have been sent Open Season because you have opted in to receive it.

Note: It may take our system up to two business days to process your unsubscribe request and during that time you may receive one or two more newsletters.

Thank you for reading Open Season.

GovExec, 600 New Hampshire Avenue NW, Washington, DC 20037

Next years 7.7% premium increase is less than the 8.7% increase of 2023, but it's still much higher than previous years. In 2022, the average enrollee increase was only 3.8%. While no one can predict the future, federal employees and annuitants should prepare to pay higher premiums and a higher rate of increase going forward.

Next years 7.7% premium increase is less than the 8.7% increase of 2023, but it's still much higher than previous years. In 2022, the average enrollee increase was only 3.8%. While no one can predict the future, federal employees and annuitants should prepare to pay higher premiums and a higher rate of increase going forward.  Some of the changes are striking. For example, the largest decrease in enrollee share of premium is from the Baylor Scott & White Standard Health Plan (A8), available in Central Texas, which costs 54% less in 2024, saving self-only enrollees around $1,500 next year. Aetna Advantage, a national PPO plan, has the same premium in 2024 as 2023. The largest increase in enrollee share of premium is from Kaiser Permanente High (F8) in the Atlanta region, which is 22% more in 2024 and will cost self-only enrollees around $1,100 more next year.

Some of the changes are striking. For example, the largest decrease in enrollee share of premium is from the Baylor Scott & White Standard Health Plan (A8), available in Central Texas, which costs 54% less in 2024, saving self-only enrollees around $1,500 next year. Aetna Advantage, a national PPO plan, has the same premium in 2024 as 2023. The largest increase in enrollee share of premium is from Kaiser Permanente High (F8) in the Atlanta region, which is 22% more in 2024 and will cost self-only enrollees around $1,100 more next year. This upcoming Open Season is a good opportunity to assess whether your current plan is still the best fit for your needs. For Basic and Standard plan members, are you enrolled in the right BCBS plan? Now might be the opportunity for you to save one or two thousand dollars a year in premium by switching to FEP Blue Focus.

This upcoming Open Season is a good opportunity to assess whether your current plan is still the best fit for your needs. For Basic and Standard plan members, are you enrolled in the right BCBS plan? Now might be the opportunity for you to save one or two thousand dollars a year in premium by switching to FEP Blue Focus.